AI Infrastructure Wars: Energy Production Defines Global Supremacy

AI energy consumption is now compounding four times faster than grid capacity additions. Which countries resolve the mismatch first will determine which countries lead in artificial intelligence over the next decade.

The constraint on artificial intelligence at scale, in 2025, is no longer model capability or chip availability. It is electricity. The rate at which AI workloads consume grid capacity now exceeds the rate at which new grid capacity is being built — by a factor of four — and the gap is widening. Which countries resolve this mismatch first will determine which countries lead in artificial intelligence over the next decade.

The numbers

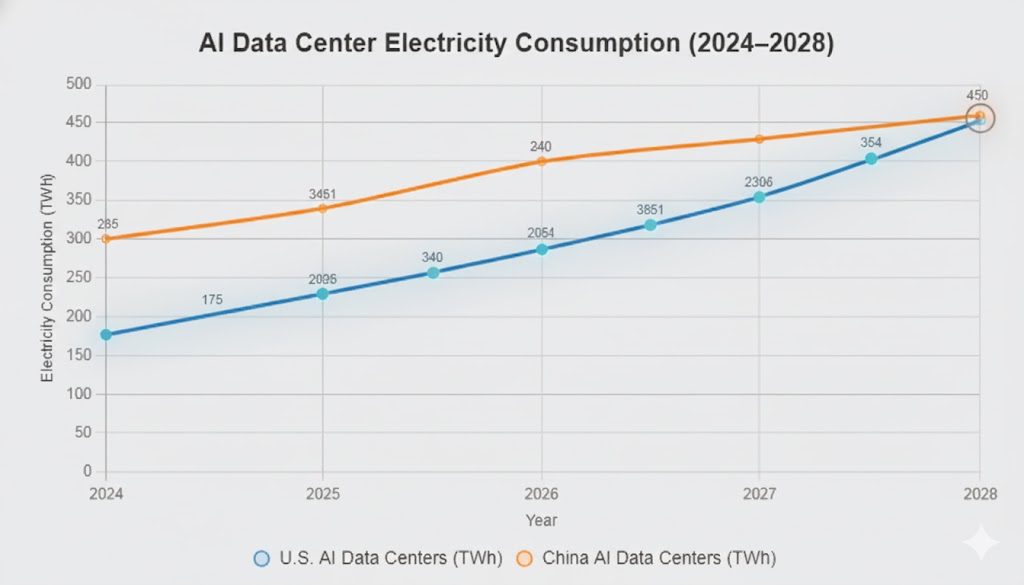

American data centers drew 176 TWh in 2024 — 4.4% of total US electricity consumption. Department of Energy projections for 2028 range from 325 to 580 TWh, the upper bound representing roughly 12% of all electricity generated in the country. Global AI-related electricity consumption is growing at 30% per year. Each Tier 5 hyperscale facility consumes 500 MW or more — equivalent to powering 375,000 homes — and the largest campuses now reach gigawatt scale.

The asymmetry is best illustrated by a thought experiment. If TikTok’s compute infrastructure were repatriated to the US, it would require hundreds of new hyperscale facilities — added to the roughly 1,000 that already exist. The cumulative load of those 1,000 facilities at maximum draw already exceeds total current US power generation. The system has no slack.

The structural mismatch

What “four times faster than grid capacity” means in practice is straightforward. Every year that AI demand grows at 30% while grid additions grow at 7–8%, the gap compounds. NVIDIA’s Jensen Huang has begun talking publicly about reliance on diesel backup. Some data-center operators are quietly siting in jurisdictions selected primarily for marginal grid capacity, not workforce or fiber.

Two structural features make this hard to fix at speed. First, transmission and substation upgrades have multi-year lead times; the binding constraint is rarely generation itself but the substations and lines that connect generation to load. Second, the physics: hyperscale AI workloads draw power at densities the existing distribution layer was not designed for. The cooling overhead alone — 30 to 40% of total facility energy — has become a meaningful design constraint.

The geopolitical layer

China’s grid produces approximately 10,000 TWh annually against the US’s 4,000 TWh, and adds another 1,000 TWh of capacity per year. By 2026, Chinese AI workloads are projected to consume roughly 400 TWh — a load the Chinese grid can absorb without breaking. The two systems are diverging not in compute (both have access to compute) but in the physical substrate compute runs on. That divergence is the new locus of strategic competition.

Where the response sits

No single intervention closes the gap. The response is layered, and the layers are where capital should be patient.

- Co-located generation. Small modular reactors sited adjacent to hyperscale facilities bypass grid bottlenecks entirely. Several US operators have announced SMR partnerships; the regulatory path remains the slowest variable.

- Semiconductor efficiency. Photonic interconnects, advanced chiplet architectures, and atomic-scale defect control collectively offer roughly an order-of-magnitude reduction in power per inference. The technology is real; the question is rate of deployment.

- Thermal management. Microfluidics and immersion cooling can compress the 30–40% cooling overhead toward 5–10%. The economics already work; standardisation is the gating factor.

- Grid intelligence. AI-native load shifting, demand forecasting, and distribution optimisation is the cheapest available intervention but the one most dependent on regulatory cooperation.

Reading

The decade’s most consequential venture-scale outcomes in the AI substrate may not come from model labs. They will come from the companies that solve the physical-layer constraints — power, thermal, network — that determine whether the next generation of AI workloads runs at all. The winners are not yet obvious. The category, in 2025, is.

Data sources: U.S. Department of Energy 2024 Report; Semi Engineering analysis; Data Center Frontier hyperscale survey.